. - upload")

Publication History

Submitted: October 02, 2023

Accepted: October 20, 2023

Published: November 01, 2023

Identification

D-0185

Citation

Asmit Raj Pandey (2023). Entry Barrier Analysis in Signal Jamming Predatory Pricing. Dinkum Journal of Economics and Managerial Innovations, 2(11):637-644.

Copyright

© 2023 DJEMI. All rights reserved

637-644

Entry Barrier Analysis in Signal Jamming Predatory PricingOriginal Article

Asmit Raj Pandey *1

- Hochschule Rhein Waal, Rhine-Waal University of Applied Sciences, Germany; asmit676@gmail.com

* Correspondence: asmit676@gmail.com

Abstract: This paper establishes a significant relation between signal-jamming predation and its entry barrier ability. Experiment was conducted considering the parameter of signal-jamming predation. From the result of this experiment, and the available data of exit ratio of new companies a binomial test was conducted. The binomial statistical test measures the test proportion with the observed proportion. In this paper, the test proportion is the exit ratio of the firm without predation and the observed proportion is the exit ratio we discover from the experiment. If signal-jamming predation is not an effective mean of entry barrier then our observed proportion should not significantly differ from test proportion. The result of this binomial test shows that there is a statistically significant relation between signal-jamming predation and its entry barrier ability. Although this result holds up with the previous belief about predation, this paper analyzes in deep about signal-jamming predation ́s entry barrier ability like very few research before. It shows in detail the reasons and rationality behind predations, its result and probable impact in the market. It is concluded that since quantities are rivals’ strategic substitutes, it is not beneficial to increase available capacity after entry. We demonstrate that incumbents that expand their capacity upon entry are more likely to crush competition, regain their monopoly, and take advantage of market power by driving up prices following the departure of their competitor.

Keywords: signal-jamming predation, entrant, entry barrier, incumbent, predation

- INTRODUCTION

Predatory pricing has given rise to a conundrum that in the past has split economists and confounded the legal system. While many economists dispute the concept of predatory pricing, there are still debates concerning its strategic implications and efficacy, which many businesses have employed. Predatory pricing is not a novel concept to firms or economists. Its use has been discussed for a while. The application of signal-jamming predation as an entry barrier is covered in this thesis work. There is never a guarantee that the new business will be profitable in the future. Here, it is assumed that the entrant determines whether or not to stay in the market based on their present earnings [1]. The incumbent, or established company, has the option to reduce the entrant’s profit by lowering prices. This move raises the likelihood that an entrant will withdraw from the market. Predation is a useful tactic in this situation since it lowers the likelihood of profit and drives competitors out of the market. Unlike other predatory schemes, like the reputation model, this one is unique. Here, the established business just aims to obstruct the entrant’s information (profit) rather than divulge any information about itself. Predation has been documented since the eighteenth century. The author [2] has demonstrated proof of predation in the Mogul Steamship Co. v. McGregor Gow and Co. case in a paper that was published. Even though there is proof of predation, Mogul Steamship was found not guilty in this instance. In the case of General Foods v. Proctor & Gamble, decided over a century later, General Foods was found not guilty of predation [3]. Nevertheless, a subsequent article by [4] has demonstrated that General Foods’ approach was, in fact, predatory. In court, these two cases were dismissed. In Mogul Steamship Co. v. McGregor Gow and Co., the traits of the predation reputation model are demonstrated, while in the General Foods case, the traits of the signal-jamming model are demonstrated. This incident happened prior to the development of an economic theory to back them up. Had there been an economic theory in existence prior to these predatory acts, the outcome might have been different. Because fresh data and research will always be helpful in addressing similar issues in the future, this work may prove vital in the near future. Even though predation is an old topic, study on it needs to be done constantly to prevent similar failures in the future. The purpose of this research is to investigate the strategic use of signal-jamming predatory pricing as an entry barrier and to monitor predatory behaviour in a laboratory setting. Using primary data from the trial, this research study was examined how signal-jamming predation is used. Information were taken from an experiment in which one person has played the role of an incumbent and the other as an entrant. These research attempts to establish a strong correlation between entry barrier and signal-jamming predation from these data. This work intends to reinforce and extend the previously established theory by [7], despite the fact that there has been little research in the area of signal-jamming predation by [5, 6]. Here, the binomial model employs experiment data to demonstrate a likely strategic use of signal-jamming predation as an entrance barrier. There is a dearth of study in this field, particularly on the entry barrier. Therefore, the goal of this research is to close the gap between the idea of signal-jamming predation and its actual implementation as an entrance barrier.

- LITERATURE REVIEW

The signal-jamming theory of predation by [8] is the main theoretical basis for this experimental research. This theory of predation is different from other as it does not depend on its reputation for predation. The main assumption of this theory is that when a new firm tries to enter a market, it is uncertain about its future profitability. Therefore, it looks at its current profit and decides whether to stay in the market or not. The entrant relies on its current profit as an indicator of future profit because the entrant`s actual demand on the market depends on a random parameter, whose value is not known by the entrant. The dominant firm with more knowledge of the market looks at this scenario and tries to deter the entry. It takes some competitive actions such as secret price cutting that will reduce the profit of the new firm. This action of price cutting not only reduces the profit of the new firm, it also effects the information that the new firm was seeking. The new firm with this price cutting strategy of the dominant firm is unable to estimate the future profitability of the market. Therefore, the dominant firm is able to distort the information that new firm is seeking. This is known as signal-jamming predation. The new firm is aware that if it enters the market, it will face fierce competition. Observing all these situations the new firm decides not to enter the market. The model presented by [9] focuses on the simplest case in which there are only two periods. The model is an example of Bayesian equilibrium where the characteristics of the dominating firm are common knowledge. In equilibrium, the dominating firm preys on the entrant and reduces its profit and that of the new firm, even when the new firm may not be fooled by the predation of the dominating firm, it leaves the market the same time he would have if there was no predation. Therefore, the dominating firm deviates from its profit-maximizing strategy to induce the exit of the new firm makes a threat of predation credible and deters the entry [10]. As per stated in the article, the model here has been expanded to include entry decision by the entrant and also has been expanded into four periods in the experiment to increase the probability of exist or entry in the market. This extension in the experiment gives the entrant time to observe the profitability and for the dominating firm enough time to distort this information that entrant is seeking [11]. There is per period uncertainty over the fixed cost in the model to eliminate the effect of learning in first period effect the second. This uncertainty has been eliminated in the experiment to remove the complication of assigning per period random fixed cost. Here, the fixed cost assigned to the entrant is same throughout the four periods. Signal-jamming theory owes much to the limit pricing and reputation literature [12]. However, there are differences between them, some of these differences are: For predation to occur the new firm has to enter the market, and asymmetric information may not be present at the predation date i.e. Incumbent price does not depend on inside information about the new company. The experimental design is based considering the following theory. The previous experiment on predatory pricing is modified to meet the theoretical basis of the signal jamming theory. The experiment conducted by Isaac and [13] and [14] has been considered and modified accordingly. The details about the theory and its modification to fit the experiment parameter are as follows:

= (, ) + (, ) (If both firms are present in market)

= (, ) + ( , ∞) (If firm two is out in the 1st period)

= Dominating firm profit when entrant is present in market and when it is not

= per period profit of the dominating firm

= Price of dominating firm in period A

= Price of the dominating firm in period B

= Price of the dominant firm at monopoly when entrant is out of market.

= Price of the new firm in period A

= Price of the new firm in period B

The above equations show the profit of the dominating firm in two periods A and B. We can see that if both the firms are present in the market then they share a profit. If the new firm is out, then dominating firm will enjoy a monopoly profit. Similarly, we also have the profit of the firm two as:

= (, ) − 𝛼 + (, ) − 𝛼 (If both firms are present in market)

= (, ) − 𝛼, (If firm two is out in the 1st period)

= New firm ́s profit when it is present in the market and out of the market

α = Fixed cost of the firm

= Per period profit of the new firm

We have taken the fixed cost into consideration because if the entrant cannot meet its fixed cost, it will not see the market as s desirable place to expand its business. The above equations show the profit of the new firm in both the period. Here the profit is per period profit deducted by the fixed cost. If the firm total profit in the first period is less than the fixed cost then, the firm is out of the market [15]. The experiment designed to fit the theoretical parameter is as follows: First, the experiment is expanded as suggested in the article. Here the different factors that lead to less entry in the market will also lead to more exit. It also gives the participants acting as an entrant enough time to understand and analyse the market. This understanding will help them in the decision-making round at the end of the experiment [16]. There are only two firms in the experiment as in the theory. This is done not only for simplicity but also a realistic approach as there is only one dominating firm that preys on the entrant. In the experiment both the firms are given certain units of production. The new firm tries to understand the market profitability and dominant firm reduces its price and tries to distort the information. Both the firms are given their maximum units of production from which they can choose their units according to their cost structure and strategy [17]. Each firm will earn their profit from the price and units sold. Since all the cost structure of a real firm cannot be involved in the experiment, the profit is taken as the difference between marginal cost and sold price. As in the theory, the dominant firms fixed cost is not considered. The new firms fixed are deducted from the profit. If the profit is below the fixed cost then firm is out of the market [18]. In the theory, the fixed cost is made uncertain and deducted in every round so that learning from one round does not affect the. The experiment here is expanded into four rounds and such approach of assigning four different fixed cost would be impossible to track and confuses the participants [19]. Therefore, here we have taken only one fixed cost that is deducted at the end of four periods. After the experiment is over, we have also included a decision-making round (as stated in article). In this round after going through four rounds of price war, the participants acting as new firm will make a decision to stay in the market or not. There has been very little research in this theory, and from an entry barrier prospective even fewer. As this theory is largely unexplored in the field of entry barrier, this thesis study aims to establish a relation between the both with this quantitative research. This experiment has expanded the signal-jamming model and included entry decision as suggested in the article by [20] to induce more exit. This increased exist along with the predatory trait will give us a clear relation that signal jamming predation acts as an entry barrier. The hypothesis of this research is based primarily on the signal-jamming theory of predation. Our aim in this thesis paper is to establish a significant relation between signal- jamming predation and its entry barrier ability to a new firm. Here, the data obtained from an experiment is tested against the previously held belief about the entry-exit ratio of a company that enters a market. If signal jamming predation is not an effective tool of predation, then the exit ratio from the experiment should not be significantly different from the average exit ratio of the new firm. To form the null hypothesis, we take a look at the previous statistical record of the exit rate in the initial years. These records will give us an idea about the average exit ratio of the new firm without predation. From the United States department of labor, we have gathered an average exit rate of the new firm. The data shows the entry and exit of the firm since 1994. From this, we have taken an average of the firm exit rate since their entry. The average exit rates of new firm in the initial two years in about 33% [21]. So, the average exit rate of the firm since 1994 is about 33%. From this, we can assume our null hypothesis that when there is no predation the exit ratio is 33%. Therefore, we can write this data into our binomial statistics as:

Ho: Signal-Jamming predation does not deter an entry of a firm.

Null Hypothesis: P = 0.33

If signal jamming predation is not an effective tool as an entry barrier, then result of the experiment should not be significantly different from the test proportion and the success probability of exit will be 33%. But, if signal-jamming predation is an effective tool of entry deterrence then we should see a significant increase in the exit ratio then normal circumstances. From this assumption about the predation, we can write the alternate hypothesis of this thesis study as:

H1: Signal- jamming predation deters an entry of a firm.

Alternate Hypothesis: P > 0.33

In order to avoid type 1 error (true hypothesis is rejected), we were taken a certain level of significance. Here, the results were compared with 1% level of significance to avoid this error. If the result is significant it was supported our alternative hypothesis.

- RESEARCH METHODOLOGY

3.1 Experiment Design

First, it is essential to create an environment that is favorable for predatory pricing to occur, more specifically signal-jamming predatory pricing to occur. In this experiment, the entrant and incumbent are in a kind of Bayesian equilibrium. There is incomplete information between the participants. The characteristics of the incumbent are common knowledge. The incumbent tries to jam the signal (profit) in order to force the entrant out of the market. In this experiment both the parties are involved in a price war with each other. It is clear that predatory pricing cannot take place with firms producing heterogeneous products, so we assume that both the parties are producing an identical product to be sold in the market. The overall demand of the market is ten units. The total demand is known to both the parties but the production capacity of an entrant is not known to an incumbent. There was also be no carryover of the production to avoid confusion. The experiment was done with two participants at a time. One was act as an entrant and other act as an incumbent. Each participant was given instructions about the experiment and assessed their cost and production. They were given an excel sheet in which they can calculate profit and loss for certain units of production. After making their calculation both participants were passed their desired units and selling price to the experiment controller. The controller then gave them result. This result were updated in their respective excel sheet and they can calculate the profit or loss they made in that period. Such price war held for four rounds. If the total profits of the entrant in these four rounds fall below fixed cost, then entrant is automatically out of the market. If not, then at the end of an experiment we have a decision-making round. In this round, the entrant after the experiment was given their decision whether to stay in the market or not. The decision along with exit ratio of participants were given us an idea of effectiveness of signal jamming predation as an entry barrier. We are aware of the fact that predation is done by a single large company. The prey can be more than one. For simplicity, we have taken only two companies in this experiment. From the literature, it is clear that predation cannot take place with two firms producing two different products. Therefore, here we assume that both firms produce a homogenous product in the market. Much of the literature is focused towards the fact that incumbent has some cost advantage over the entrant. In this experiment, our overall cost structure is represented graphically as:

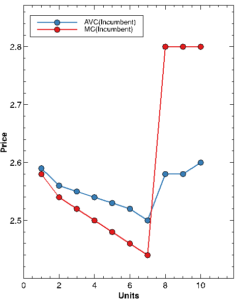

Figure 01: Cost structure of the incumbent

Figure 02: Cost structure of the entrant

As the cost structure suggests incumbent being the dominant firm has the capacity to produce the full demand of the market. The entrant, on the other hand, has a small advantage, as when the incumbent decides not to produce more than seven units then it still has three units from market demand that it can make profit from. The competitive equilibrium occurs where incumbent produces seven units and entrant produces three units. At this point, both the firm has lowest marginal and average variable cost. This would be the ideal and rational pricing point for both the company. If the incumbent decides to produce eight units then entrant still has some opportunity to make profit. However, entrant profit reduced because of increasing marginal cost. At this point (when incumbent produces more than seven units) we can clearly see the incumbent deviating from its equilibrium to reduce the entrant ́s profit and jam the signal. The literature seems to be divided on what can be considered predatory. The literature considered for this experiment [22] has not clearly defined the price that can be considered predatory. However, here in this experiment, we considered the point lower that Price lower than 2.65 or producing more than seven units as predatory. At this point, we can see the incumbent can restrict the entrant from the market but by posting below its marginal cost or deviating from its equilibrium. This can be said as a predatory behavior because the incumbent is purposely taking a loss to force the exit of a new company. Deep pocket theory or the long purse theory is often associated with predatory pricing. The predator can finance its predatory approach from the profit it generates from other branches. However, this approach can also be associated with any other case of predation such as the reputation. Even when the financial power is given to entrant, it will not affect the profit of the firm, which is the most important driving factor behind entrant staying or leaving the market. In this experiment, there is no prior financial strength given to the predator or the entrant. The literature is focused on the fixed cost of the entrant. If the profit falls below the fixed cost than entrant is forced to exit a market. In the experiment, total profit was calculated at the end of the experiment. Here, if the profit falls below fixed cost, the entrant is automatically out of the market. However, if it is higher than fixed cost then the participant was made an entry decision. The decision of the participants and automatic exit from the experiment proved the effectiveness of entry barrier from signal jamming predation. In this experiment recoupment phase is not involved to avoid confusion. Due to several limiting factors such as having no buyers in the experiment and financial constraints this phase in not present in the experiment. The literature is again divided on the overall information status in predatory pricing. Experiment on predatory pricing such the “Predatory pricing in a multiple market experiment” by [23], have achieved successful predatory behavior where complete information was lacking. In this experiment, we have incomplete information status where one firm preference affects the payoff of the other. The overall cost structure of one party were unknown to the other party. The total demand in the market was known to both the firm, but the total production capacity of entrant was unknown to another party. The incumbent having some information advantage knows that entrant was exit if the profit is lower than fixed cost. But the exact amount of fixed cost was unknown to the incumbent. In this experiment sellers (incumbent and entrant) post certain quantity at a certain price to be sold in the market. In each period maximum of 10 units are sold. The quantity that was sold depends on the revealed preference. The profit is calculated as the difference between sold price and the marginal cost. The firms that post a lower price for its product were sold in the market. Example: Incumbent can post 2.6 euro for 8 units. In this case, incumbent 8 units are sold and entrant 2 units are sold. An important point to note here is that when entrant`s 2 units are sold then its selling price was not be the one posted earlier but at the marginal cost of production of 2 units = 2.56. The firm that posts the higher price was not received any profit for that period. This can be justified as a law of demand and supply. The overall demand of the market is 10 units and total supply in the market being 11 units, the price was drop down. The price of incumbent already below the entrant was stay the same, whereas the prices of the entrant being higher fall down.

3.2 Data

The sample proportion, also known as the observed proportion, makes up the second half of our data. A total of 26 people, split into entrant and incumbent groups, participated in the experiment to collect this data. The signal jamming theory served as the foundation for the experiment, and the design is as mentioned above. A new company’s entrance into the market or its departure was the outcome of these participants’ battle for a shared market. This experiment was designed to find out if the exit ratio is substantially higher or lower than the test proportion. The outcome of these findings was greatly influenced by the participants. Nearly all of them had solid economic backgrounds, which contributed to a better comprehension of the experiment that was carried out. Each participant received an explanation of their role before to the experiment, and they were all given the identical introduction to read before the trial began. There were thirteen sets of experiments, with two participants in each set. The participants were housed in a different compartment to ensure the independence of the data. Throughout the trial, they were prohibited from speaking to any other participants or to each other. They were given their company’s cost structure, which they used to determine the units and selling price. Using the excel spreadsheet that was given to them, they were able to determine their profit and loss. They scribbled their selling units on a sheet of paper and gave it to the experiment coordinator after figuring out their profit. The organiser selected the winner of each round by examining the selling price and selling units. The coordinator then gave each participant access to the sales results, which they updated on their computers. Each participant in the procedure underwent four rounds. The outcome was determined at the conclusion of the fourth round. Since this is a predatory pricing entry deterrence experiment, the incumbent’s ability to prevent entry is what counts as success, and its inability to do so is what counts as failure. The experiment’s outcomes are listed below:

Table 01 : Experimental response

| Participants | Experiment Results | Results |

| 1-2 | Entry Deterrence | Success |

| 3-4 | Entry Deterrence | Success |

| 5-6 | Accommodation | Failure |

| 7-8 | Entry Deterrence | Success |

| 9-10 | Entry Deterrence | Success |

| 11-12 | Entry Deterrence | Success |

| 13-14 | Entry Deterrence | Success |

| 15-16 | Entry Deterrence | Success |

| 17-18 | Entry Deterrence | Success |

| 19-20 | Accommodation | Failure |

| 21-22 | Accommodation | Failure |

| 23-24 | Entry Deterrence | Success |

| 25-26 | Entry Deterrence | Success |

The experiment’s result is displayed in table 1. Nine of the thirteen observations successfully prevented the ingress by using predation through signal jamming. After surviving the predation stage, four people chose to remain in the market. Every person acting as an incumbent posted a quantity that can be deemed predatory, as previously indicated (greater than 7units). With the exception of participant 19–20, every incumbent posted a predatory pricing. The only other player who didn’t post a predatory pricing was this one. This finding indicates that predation is a behaviour attribute that exhibits in a regulated setting. Additionally, we witness participants straying from equilibrium and suffering a loss in order to compel the new firm to close. The aforementioned outcome amply demonstrates how successful signal jamming predation is. This outcome, though, might not be noteworthy. We will use the binomial statistical test to examine its significance. Appendix B displays the specifics of each participant’s price and quantity for each round, as well as the choices made by those who wished to remain in the market.

- RESULTS AND DISCUSSION

The outcome of the binomial test between the test and observed proportions is discussed in this section. The null hypothesis provides the test proportion, and our experiment’s data represents the observed proportion. Through statistical testing, we may determine whether to accept or reject our null hypothesis based on the results. The following is the outcome of the binomial statistical test:

Table 02: Statistical result from the binomial test

| Binomial Test | |||||

| Category | Number of Observation | Observed Proportion | Test Proportion | P-Value | |

| Group 1 | Deterrence | 9 | 0.69 |

0.33 |

0.08 |

| Group 2 | Accommodation | 4 | 0.31 | ||

| Total | 13 | 1.00 | |||

The outcome of our test is displayed in Table 2 above. It is evident that the test proportion is lower than the observed proportion. This is because we entered the trial with a 9 out of 13 entry deterrent. A statistical test is conducted between this result and the test proportion. The outcome provides us with a P-value, or probability value, of 0.008. The probability that the observed value happened by chance is indicated by the value of p, which is always between 0 and 1. Here, the statistical significance of our observed result is demonstrated by the low P-value of 0.008. In order to assess our type one error value, we have selected a significance level of 1%. Based on the results above, we can conclude that: P: 0.008 <0.01. Our observed result is statistically significant at the 1% level of significance, as indicated by the P-value being less than 1%. Thus, based on the aforementioned finding, we may declare that our alternative hypothesis—that signal-jamming predation deters an entry—will be accepted and our null hypothesis—that signal-jamming predation does not deter an entry—can be rejected. We will carefully examine the outcome from the above table in this discussion. In addition to demonstrating that the P-value is 0.008, which indicates statistical significance, it also demonstrates how strongly our alternative hypothesis is supported by the observed outcome. Binomial distribution statistics is used to assess the relationship between our observed proportion and our test proportion. We can see from this probability distribution that our result lends credence to our alternative theory. The study’s findings are consistent with the widespread belief that predation through signal jamming prevents access. Like any study, this one has a number of limitations. Financial constraints forced it to run during the experiment; also, the welfare impact of signal-jamming predatory pricing from this study has not been examined, and there were few observations made during the trial. While the empirical work concentrates on a small number of situations, previous theoretical literature examines comparable contexts under somewhat specific assumptions [23].

- CONCLUSION

The ability to create an entry barrier and signal-jamming predation are significantly correlated, as this article demonstrates. The experiment was carried out with signal-jamming predation as a consideration. A binomial test was carried out using the experiment’s outcome and the information on the exit ratio of newly established businesses. The test proportion is compared to the observed proportion using the binomial statistical test. The exit ratio we find from the experiment is the observed proportion in this paper, and the test proportion is the exit ratio of the company without predation. Our found proportion shouldn’t deviate noticeably from the test proportion if signal-jamming predation isn’t a useful mean of entry barrier. This binomial test’s result indicates that the capacity of signal-jamming predation to create an entry barrier is statistically significant. While the results support the earlier hypothesis regarding predation, this work examines in detail the entrance barrier capabilities of signal-jamming predation in a way that very few prior studies have done. It provides a thorough explanation of the motivations and logic of predations, as well as their outcome and likely market influence. It is determined that increasing available capacity after entry is not advantageous because quantities are competitors’ strategic alternatives. We show that market leaders that increase their capacity at the outset have a greater chance of stifling competition, regaining their monopoly, and abusing their market dominance by raising prices after their rivals leave.

REFERENCES

- Besanko D et al (2004) Economics Of Strateg John Wiley and Sons, New Jersey

- Bolton P, Brodley J F, and Riordan M H (2000) Predatory Pricing: Strategic Theory and Legal Ploicy. The Goergetown Law Journal 88: 2239

- Cheng, H. F. G. (2020). An economic perspective on the inherent plausibility and frequency of predatory pricing: the case for more aggressive regulation. European Competition Journal, 16(2-3), 343-367.

- D’Souza, E., & Dev, P. (2019). Capital Market Predation in the Indian Internet Commerce Sector.

- Federal Trade Commission (1984) Dismissal Order, Docket 9085. New York: Federal Trade Commission. https://www.ftc.gov/sites/default/files/documents/commission_decision_volumes/volume- 103/ftc_volume_decision_103_january_-_june_1984pages_204-373.pdf. Accessed 5 September 2017

- Fudenberg D, and Tirole J (1986) A “Signal-Jamming” Theory of Predation. The RAND journal of Economics 17(3):366-376

- Harrison G N (1988) Predatory pricing in a multiple market experiment. Journal of Economic Behaviour and Organization 9(4):405-417 Pim Martens & Gerjo Kork (2023). Literature Review on Multidisciplinary Approaches to Waste Management: Principles and Variables Associated with Environmentally Friendly Consumer Behavior. Dinkum Journal of Economics and Managerial Innovations, 2(10):596-602.

- Hollander M, Wolfe D A (1999) Nonparametric Statistical Method. John Wiley & Sons Inc, New York

- Hüschelrath K (2009) Competition Policy Analysis: An Integrated Approach. Physica-Verlag, Heidelberg

- Isaac R M, Smith V L (1985) In search of predatory pricing. Journal of political economy 93(2):320-345

- Jung Y J, KagelJ H (1994) On the existence of predatory pricing: An Experimental study of Reputation and Entry Deterrence in Chain-Store Game. The Rand Journal of Economics 25(1):72-93

- Laws (2020) Standard Oil Co. of New Jersey V. United State http://constitution.laws.com/supreme-court-decisions/standard-oil-co-of-new-jersey-v-united-states. Accessed 1 April 2023

- Muhammad Nadeem Asghar & Ali Jalil Obaid (2023). Review of the Research on Managerial Accountancy’ Function in Sustainability Reporting and Accounting Dinkum Journal of Economics and Managerial Innovations, 2(10):603-609Original Article

- Pike C (2016) Summary of discussion on the roundtable on price discrimination No 15. https://one.oecd.org/document/DAF/COMP/M(2016)2/ANN3/FINAL/en/pdf. Accessed 1 April 2023

- Rasumsen E (1997) Signal Jamming and Limit Pricing: A Unified Approach, In Public Policy and Economic Analysis. Kyushu University Press. http://rasmusen.org/published/Rasmusen_97BOOK.jamming.pdf. Accessed 2 April 2023

- Snedecor G W, Cochran W G (1976) Satistical Methods. The Iowa State University Press, Iwoa

- United States Department of Labor (2016) Bureau Of Labor Statistics. https://www.bls.gov/bdm/entrepreneurship/entrepreneurship.htm. Accessed 17 September 2017

- Varian H R (2006) Intermediate Micro Economics. W. Norton & Company, New York

- Yamey B S (1972) Predatory price cutting:Notes and comments. The Journal od Law & Economics 15(1): 129-142.

Publication History

Submitted: October 02, 2023

Accepted: October 20, 2023

Published: November 01, 2023

Identification

D-0185

Citation

Asmit Raj Pandey (2023). Entry Barrier Analysis in Signal Jamming Predatory Pricing. Dinkum Journal of Economics and Managerial Innovations, 2(11):637-644.

Copyright

© 2023 DJEMI. All rights reserved